Trusted by 100+ companies worldwide across the agri and dry bulk market

For importers, exporters, feed compounders and flour mills, CM Navigator is the agricultural commodity trading platform that brings pricing, freight and trade flows into one place.

Outcome: Faster origin decisions. Clearer margin visibility. More confident execution.

CM Navigator Platform supports a wide range of grains.

Agricultural grains & oilseed, barley, beans, corn, DDGS, faba beans, faba hull pellets, lentils, linseed, lupins, malt, oats, peas, rapeseed, rapeseed meal, rye, sorghum, soybean, sunflowerseed, triticale, wheat, wheat bran pellets.

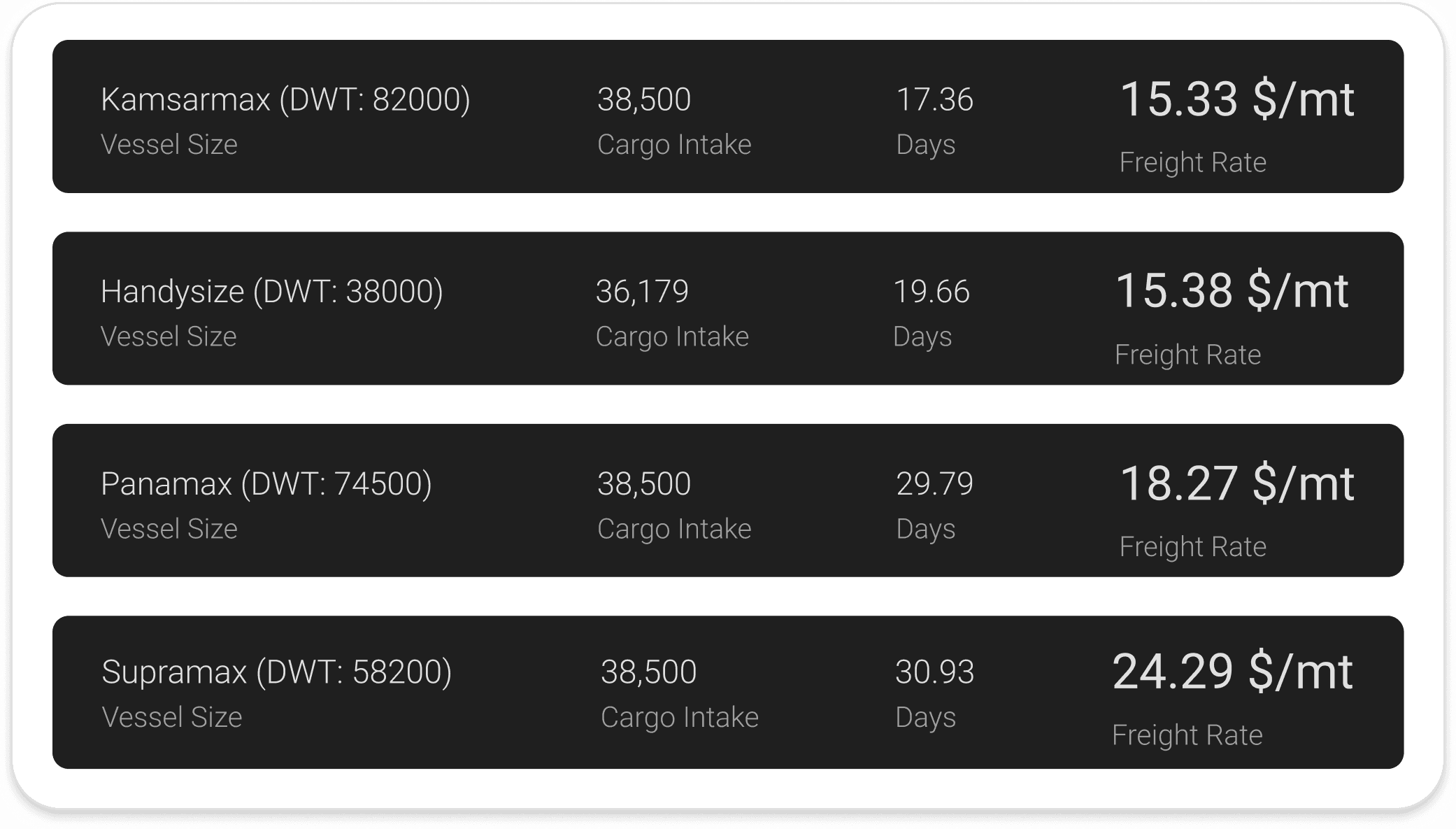

Our Freight Calculator feature supports a wide range of dry bulk commodities, including:

Yes. Data can be exported or accessed via API, allowing custom dashboards, spreadsheets, or internal models to be built using CM Navigator's live data.

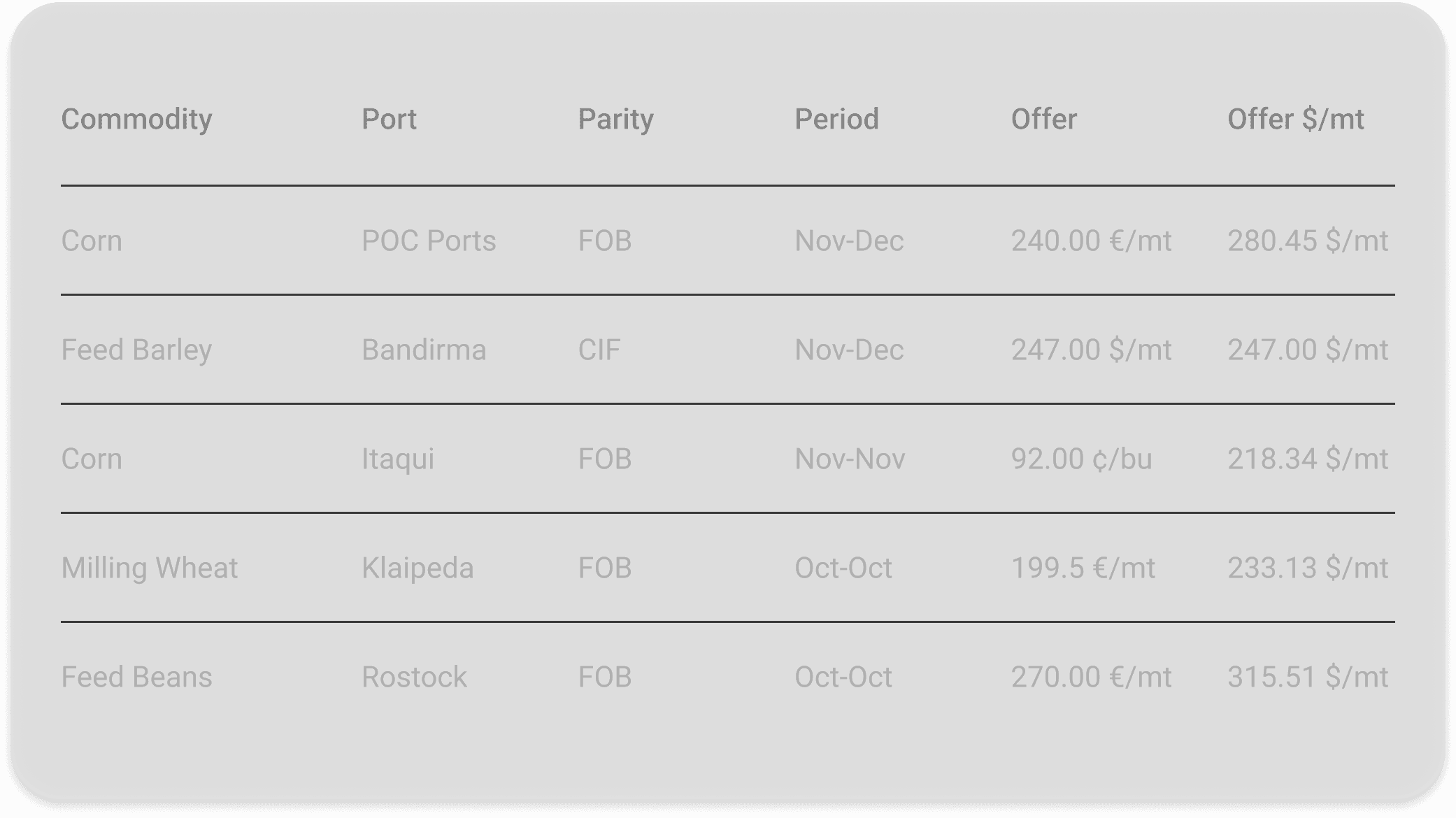

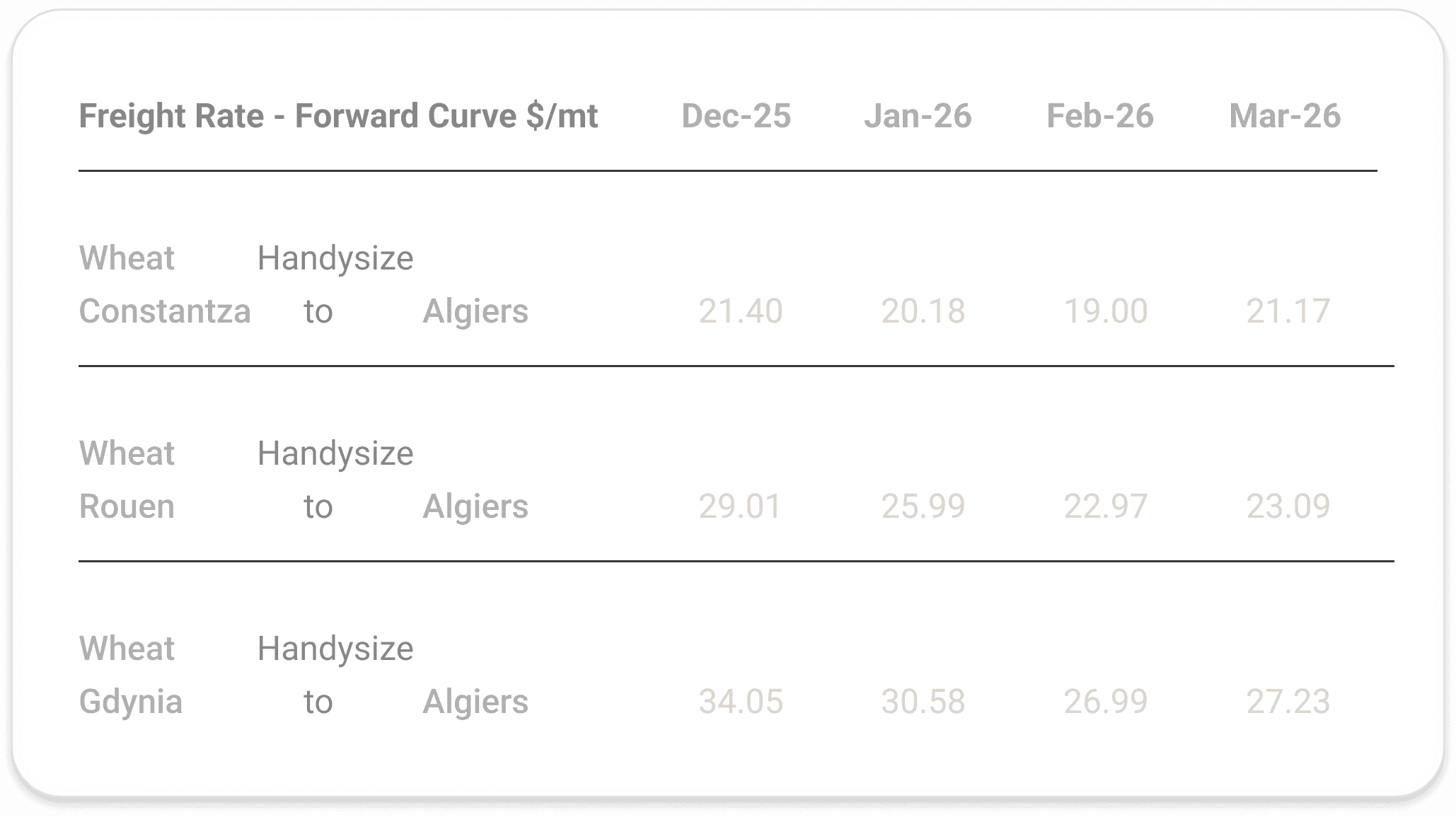

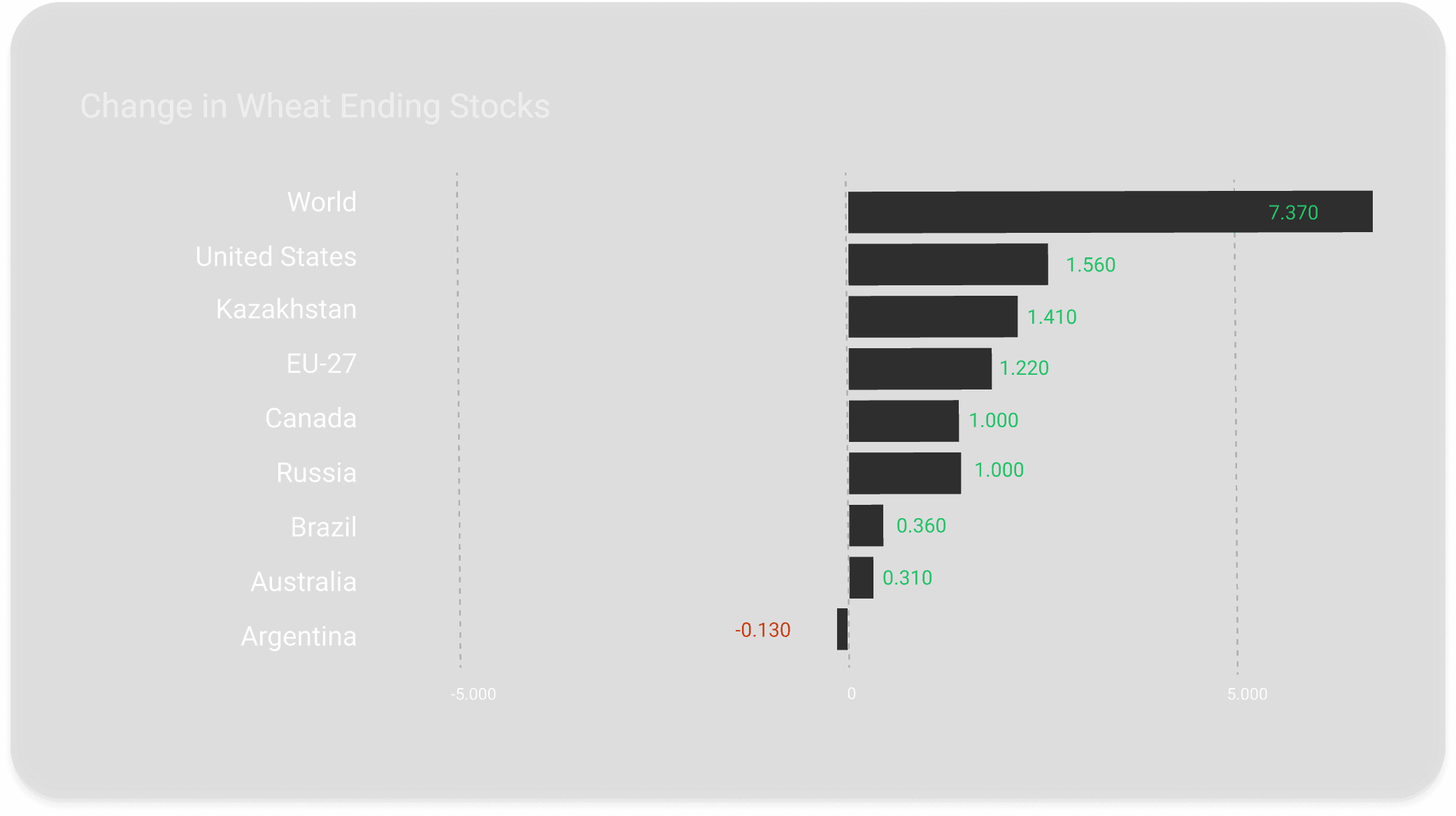

CM Navigator’s data is continuously verified by our in-house brokers and analysts. Live market prices, bids, offers, and freight rates are updated daily. Prices reflect actual tradable levels, not just estimates. Supply and demand forecasts adjust dynamically with market events (weather, geopolitics, crop inspections).

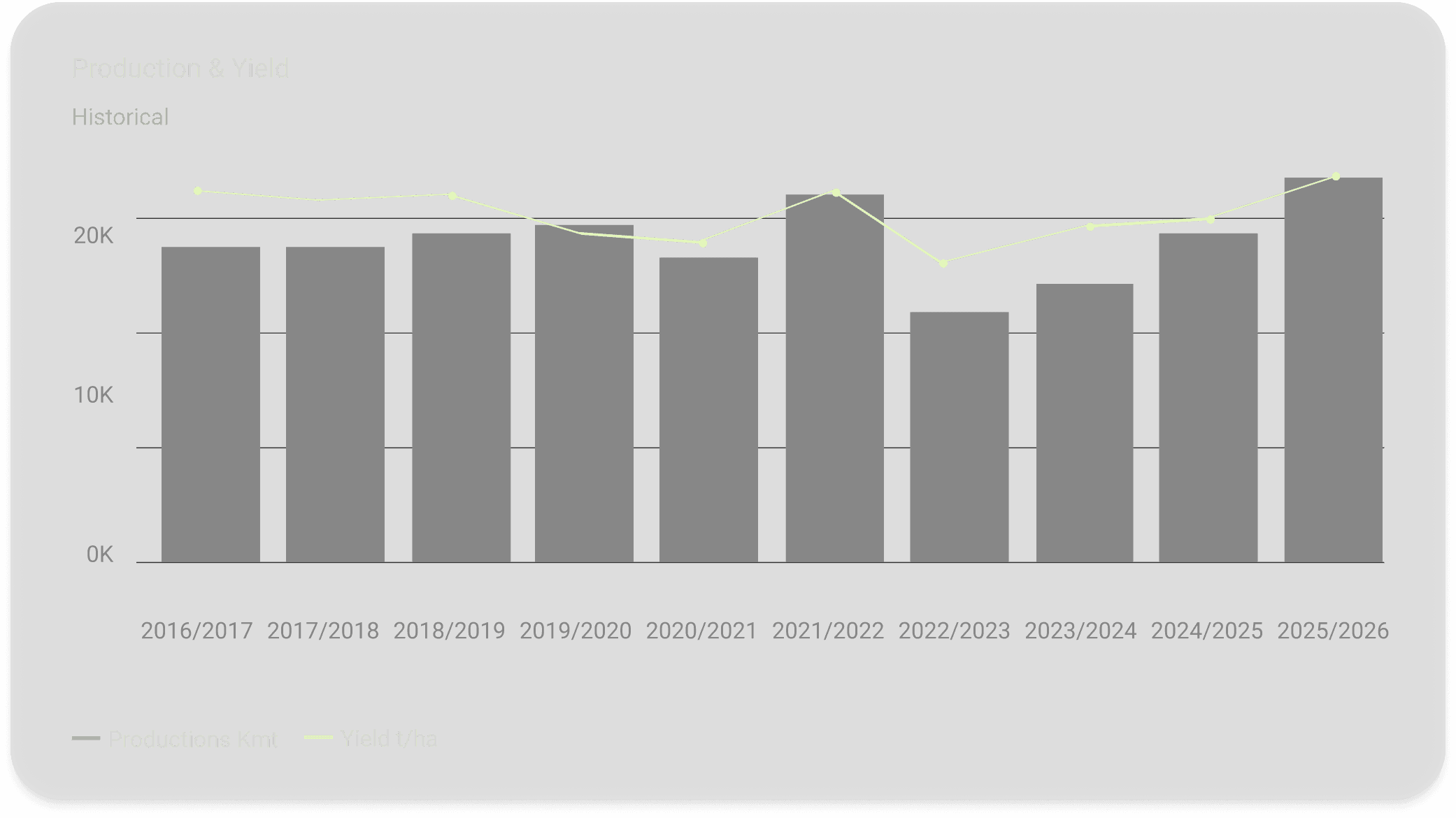

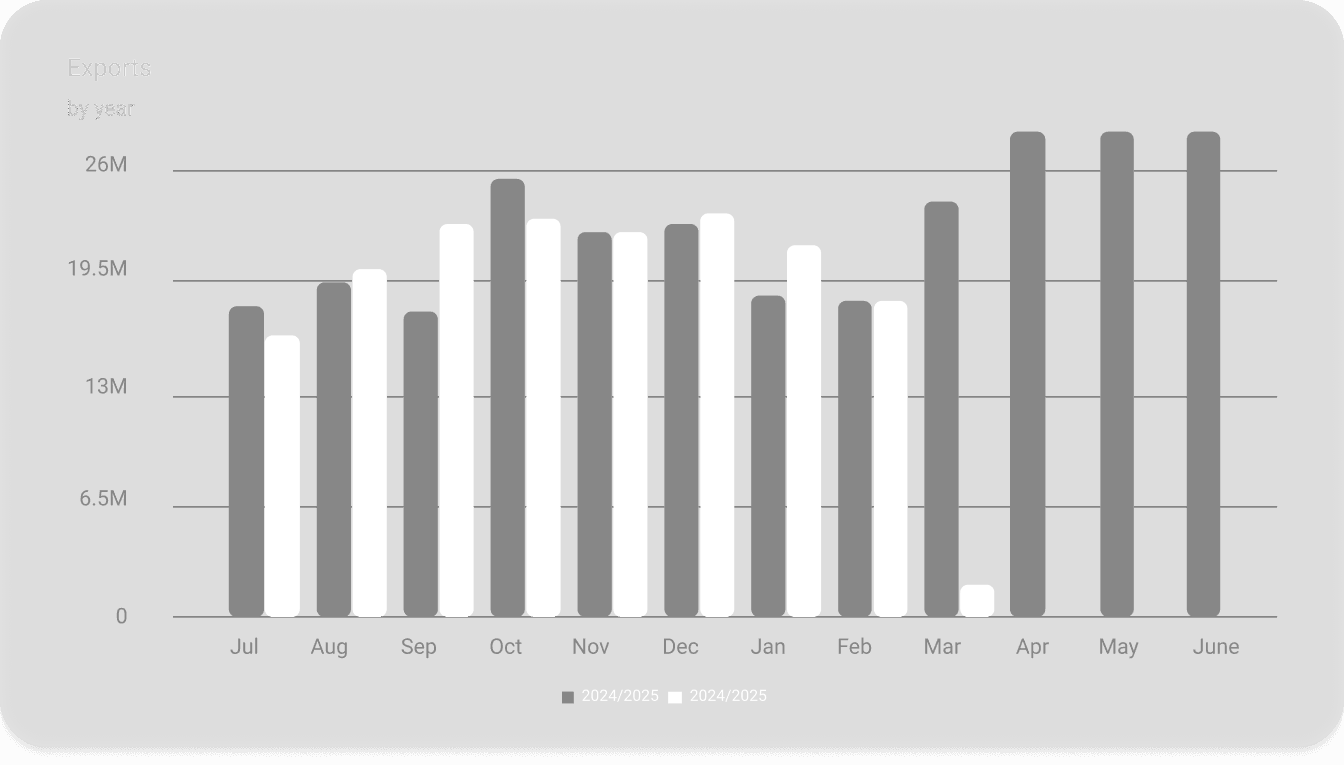

Yes, CM Navigator maintains a comprehensive historical database for market prices, freight rates, supply and demand forecasts, and CFR and FOB values.

Yes, we offer a 7-day free trial with full access - no commitment required. You can also request a guided demo to see the platform in action.

We cover all major grain export regions, including:

Commodity market intelligence is real-time data and analysis covering prices, freight rates, supply and demand, and trade flows for physical commodity markets. CM Navigator delivers this intelligence in one platform - so physical agri traders can make faster, better-informed decisions.